Positive jobs data supported the market last week. The U.S. establishment survey indicated 372,000 new jobs were created in June. The rally was broad-based as every sector added jobs last month except for the governmental sector. Health care, professional and business services, and leisure and hospitality marked the highest gains (Figure 1).

Key Points for the Week

- The U.S. economy produced 372,000 new jobs last month as every non-governmental sector added jobs.

- Unemployment remained at 3.6%. The household survey indicated workers are no longer returning to the labor force even though more than 11 million jobs remain unfilled.

- Home equity lines and credit cards are becoming more common tools for managing cash flow as interest rates have increased and government aid programs have wound down.

The household survey indicated the number of people reentering the labor force is starting to slow. The participation rate dropped slightly last month and seems to have leveled out after steady increases through the post-pandemic recovery. This trend confirms our view that the pandemic caused some people to retire early or exit the labor force for other reasons. Unemployment remained at 3.6%, and average hourly earnings climbed 5.1%. Non-managerial workers’ wages are rising most rapidly. They are 12.6% higher than one year ago and rose 1.0% last month.

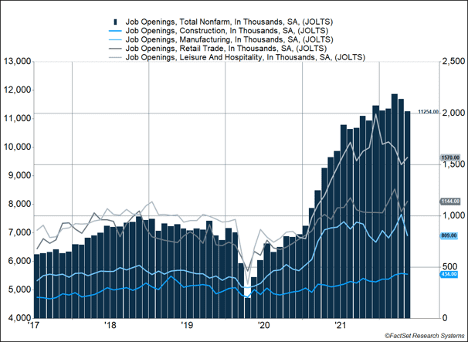

The Job Openings Labor Turnover Survey (JOLTS) indicates companies are pulling back unfilled job applications at a slow rate despite interest rate hikes designed to slow the economy. Job openings dropped 427,000 in May as declines in manufacturing and professional and business services eased demand. The Federal Reserve may have preferred further reductions in labor demand as an indication that inflation pressures are declining (Figure 2).

The S&P 500 recovered 2.0% last week, supported by the strong jobs data. The MSCI ACWI added 1.6%. Bonds reversed recent gains. The Bloomberg Aggregate Bond Index fell 0.9%. The Consumer Price Index leads a busy list of data releases this week as earnings season accelerates.

Figure 1

Figure 2

Job Growth, Participation, and Rates

Good news for workers makes it more likely the Federal Reserve will raise rates 0.75% at its meeting in late July. Last week, the government released three major job reports, and all three pointed to ongoing strength in the labor market. The June establishment report indicated the economy continues to produce a large number of jobs. The household survey shows the COVID-driven reassessment of life has cemented a reprioritization of work that has caused some to leave the labor force. The JOLTS data show openings are headed lower, but not fast enough for the Fed to slow its plan for higher rates.

Establishment Survey

Jobs growth was robust in June. Payroll data indicated the U.S. added 372,000 jobs, beating expectations by nearly 100,000. Previous months were revised lower by 74,000. Even counting the revisions, job growth was higher than expected. It has also been consistent the last four months, which all produced between 350,000 and 400,000 jobs. That means new job entrants are finding jobs relatively easily and more people are returning to positions. With the gains, 98% of the jobs lost in March and April of 2020 have now been recovered (Figure 1).

The underlying data showed broad labor market strength. Every major private sector industry added jobs, with health care and leisure and hospitality producing the most. Manufacturing added 29,000 jobs and now employs more people than before the pandemic. Government employment, which is often affected by educational hiring, was the only sector that lost jobs.

Household Survey

The household survey showed similar trends. Unemployment held steady at 3.6%. The household survey suggested employment and the labor force both shrunk. Fewer households working pushed the participation rate down to 62.2%, well short of the pre-crisis level of 63.4%. After a steady number of people rejoined the labor force as the economy reopened, the participation rate has stalled at about 1% below pre-pandemic highs.

JOLTS

The JOLTS report for May was also released last week. Job openings fell 427,000 to 11.3 million, which was 200,000 higher than expectations. Manufacturing and professional and business services declined 208,000 and 325,000, respectively. The ratio of job openings to unemployed workers declined to 1.89. The Fed would like to see excess demand for labor decline, and the large quantity of open positions suggests this isn’t happening very quickly (Figure 2).

The Fed

Minutes from its most recent meeting suggest the strong jobs data will support the hawkish Fed raising rates 0.75% later this month. The Fed is concerned about its credibility and looks intent on suppressing inflation quickly. In its minutes, the Fed noted, “many participants saying that a significant risk now facing the Committee was that elevated inflation could become entrenched if the public began to question the resolve of the Committee to adjust the stance of policy as warranted.”

About the only data point left that may cause the Fed to slow is the Consumer Price Index, which will be published this week. It is possible significantly smaller-than-expected price increases could cause the Fed to back off and only raise rates 0.5%.

Last week’s releases leave us better off than a week ago because the economy looks more capable of weathering increased rates without going into a recession. The Fed’s path to taming inflation while avoiding a recession is still narrow, just a little wider than it was before.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

US Bureau of Labor Statistics, 7/8/2022. https://www.bls.gov/news.release/empsit.nr0.htm

US Bureau of Labor Statistics, 7/6/2022. https://www.bls.gov/news.release/jolts.nr0.htm

Federal Open Market Committee. 06/14/2022. https://www.federalreserve.gov/monetarypolicy/files/fomcminutes20220615.pdf

Compliance Case # 01425380